One growth market in the UK in recent years has been private healthcare insurance. A handful of FTSE companies are benefitting from this rising trend, including insurance giant Aviva. Last year, the firm reported that its health insurance sales surged 41%.

Aviva CEO Amanada Blanc said: “We’ve seen individuals looking at the NHS and saying: ‘I can afford to buy health cover, so I will do that.’ So we’ve definitely seen a take-up in individual policies. We’ve also seen small businesses take advantage of the opportunity to protect their employees.”

That’s a reference, of course, to the NHS’s massive backlog of cases. In June, the waiting list reached 7.62m, with the median waiting time for treatment at 14.3 weeks (almost double the pre-pandemic wait).

The new government has called the NHS a “broken” system (though not “beaten“) following years of underinvestment. Things aren’t expected to improve anytime soon, especially with budget pressures and a rapidly rising (and ageing) population.

So the steady growth of private healthcare, which is carrying out more outsourced work for the NHS, seems almost certain. Here’s one FTSE 250 stock that offers investors direct exposure to the trend.

Booming demand

Spire Healthcare Group‘s (LSE: SPI) the second-largest provider of private healthcare in the UK. It runs 38 hospitals and over 50 clinics, medical centres and consulting rooms.

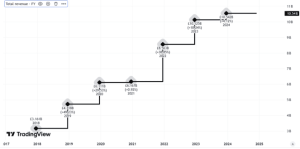

The share price is up 84% in five years, giving the firm a £903m market-cap.

The company’s carrying out more work for the NHS and benefitting from both people and businesses paying to avoid long waiting lists. In 2023, revenue rose 13.4% to £1.35bn, while adjusted pre-tax profit rocketed 175% to £38.8m. Free cash flow increased 71.4% to £48m.

This strong performance continued into the first half of 2024. Spire’s revenue rose 12.7% to £762.5m, and adjusted pre-tax profit jumped 20.2% to £26.8m. Growth was boosted by the acquisition of Vita Health Group, a leading provider of mental and physical health services.

NHS revenue increased 5.2%, and the average revenue per case rose 4.7% to £3,495.

For the full year, revenue’s set to jump around 12.3% to £1.53bn. And the firm’s now fully staffed at almost all sites, which should help reduce the need for expensive agency staff.

CEO Justin Ash said: “Spire stands ready to work with the new government to help address NHS waiting lists.”

Valuation

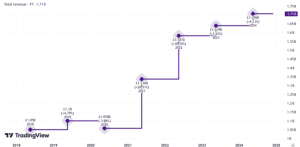

Looking further ahead, forecasts show steady if unspectacular growth through to 2026.

| Revenue | |

|---|---|

| 2023 | £1.35bn |

| 2024 | £1.53bn |

| 2025 | £1.62bn |

| 2026 | £1.72bn |

One risk here would be a government U-turn on using the private sector to bring down NHS waiting lists. This doesn’t look likely to me, but it can’t be ruled out.

Another issue is that the stock looks expensive, trading at 26 times trailing earnings. However, analysts see profits growing much faster than revenue, resulting in a cheap forward earnings multiple of 11 for 2026.

There’s also a dividend set to grow rapidly, though the yield‘s currently tiny at just under 1%.

Pure-play stock

According to Spire, more young people than ever are opting for private health insurance. This suggests going private could become the norm for a new generation, even after NHS waiting lists are reduced.

If I wanted pureplay exposure to this theme in my portfolio and had the cash, I’d consider buying shares of Spire Healthcare.

This post was originally published on Motley Fool