The National Grid (LSE: NG) share price is never going to shoot the lights out. That’s not why investors invest in the power giant.

The main attraction is the dividend. Investors typically expect to get income of around 5.5% a year, with any share price growth seen as a bonus.

It’s possible to find higher yields, but few seem more dependable than this. National Grid is a regulated monopoly, and we have a pretty shrewd idea how much money it is going to make, and how sustainable the dividend is likely to be.

That allows the group to get away with startlingly low dividend cover of just 1.1. With most companies, investors prefer to see a dividend covered twice by earnings. National Grid gets a free pass here — although having just checked, dividend cover is better than I expected at 1.4. Which is nice.

This dividend stock smashes the FTSE 100 average

Today’s yield is nice too, at 5.79%. That’s comfortably above the average FTSE 100 average of 3.64%.

Over time, the difference adds up. A 5.79% yield would turn £10,000 into £30,824 over 20 years, while a 3.64% yield would deliver £20,443. That’s almost £10k less. Obviously, I’ve not included share price growth in this.

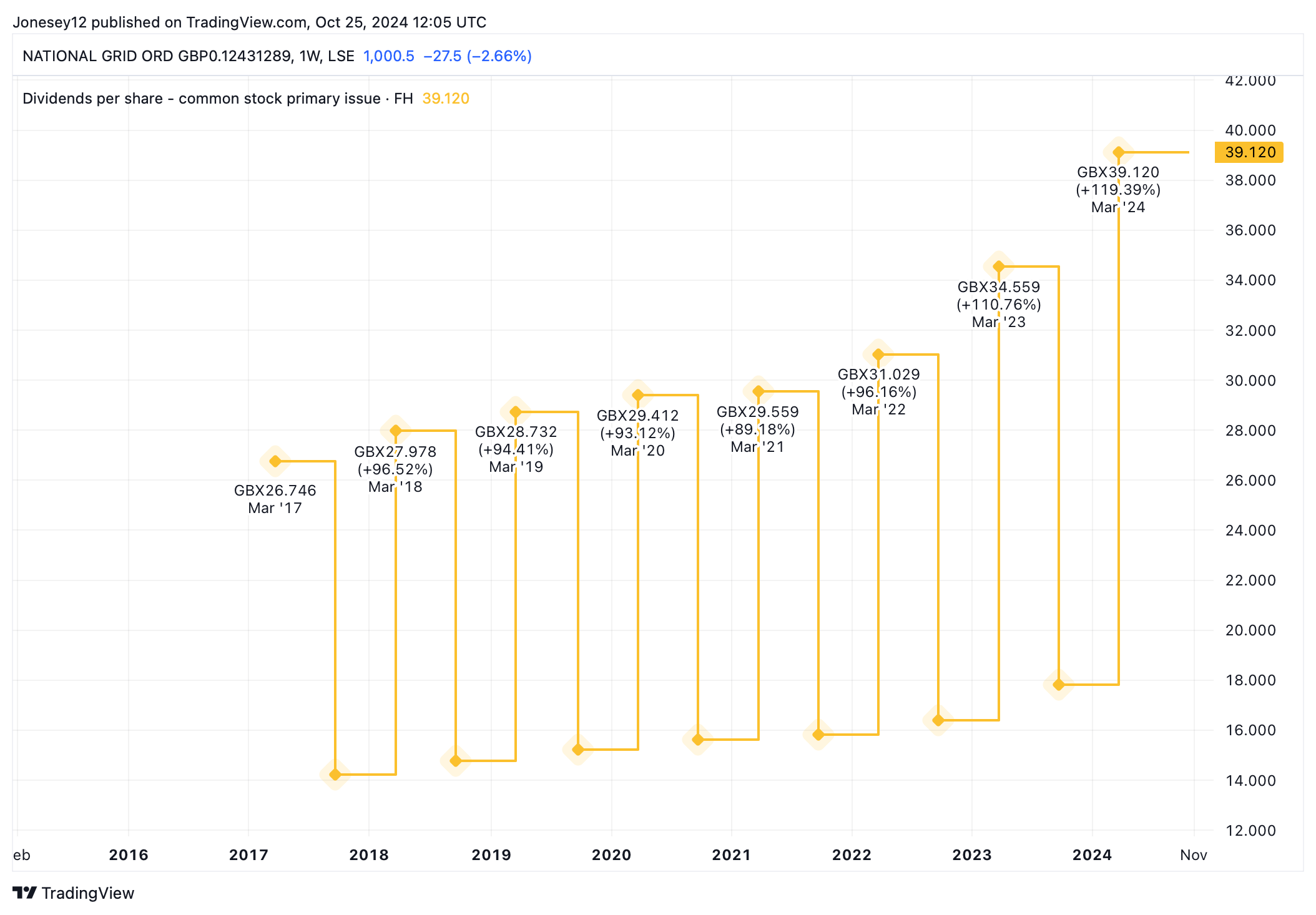

Better still, National Grid has a history of steadily increasing its dividend over time, including during the pandemic. Let’s see what the chart says.

Chart by TradingView

The share price hasn’t done too badly, either. It’s up 13.02% over the last year, and 18.34% over five. It’s beaten the FTSE 100, just, which is up 11.30% and 12.67% over those timescales.

No share is without risk, not even this one. National Grid shares plunged more than 10% on 23 May, after the board announced a £7bn rights issue to fund energy infrastructure investment. Once they got over their shock, investors piled in.

I’m worried about its debt

National Grid still looks decent value, judging by the price-to-earnings ratio. Typically, the P/E hovers around 15 times, the figure investors traditionally view as representing fair value. Today it’s notably below that at 12 times.

So can it deliver share price growth, too? The 13 analysts offering one-year share price forecasts have set a median target of 1,122.5p. That’s up 12.16% from today’s level, if it happens. Throw in the yield, and that’s a solid total return.

Yet National Grid worries me, and I won’t buy it. I keep stumbling over its net debt, which is forecast to hit £41.9bn in 2025 then £46.73bn in 2026. That’s close to today’s market cap of £48.93bn.

Labour is keen to accelerate the green transition but building UK infrastructure is notoriously slow and expensive. I wouldn’t rule out National Grid coming back for another rights issue in the next few years.

I’m suspect National Grid may struggle to fund a rising dividend at the same time. And as I said, that’s the main attraction.

I’ve been saying this for some time and yet National Grid investors have done nicely by going their own way. I’m still not joining them, though.

This post was originally published on Motley Fool