The Rolls-Royce (LSE:RR) share price is up 173% over 12 months, and even more over two years. It’s a company that returned from the brink, with some analysts forecasting that it would never truly recover from its pandemic-induced struggles.

However, UBS analysts were among those highlighting that the stock was vastly undervalued, noting in August 2023 that Rolls could find fair value around 600p. So what are UBS and its peers saying now about Rolls-Royce?

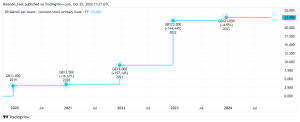

Above target

Rolls-Royce is now trading above its share price target. The consensus of all the analysts covering the stock suggests that fair value would be 535p a share.

This can mean several things. Firstly, it can often suggest that analysts think the stock’s overvalued, but that’s not reflected by the ratings — there are eight Buys, four Outperforms, three Holds, one Underperform and one Sell.

Instead, it may be the case that the share price and the business are moving so fast that analysts are simply struggling to keep up.

The most recent of ratings have struck a positive tone. For example, UBS analyst Ian Douglas-Pennant reiterated his Buy rating on October 8, maintaining a target price of 640p.

What about earnings?

Well naturally, Rolls-Royce stock’s resurgence over the past two years has been accompanied by improving earnings and positive sentiment about future earnings.

Analysts expect Rolls to deliver 17.7p a share in 2024, and this then rises to 20p in 2025 and 23p in 2026. This means the engineering giant’s trading at 31.7 times earnings for 2024, and then 27 times for 2025, and 24.4 times for 2026.

Analysts are also expecting a 1% dividend yield.

Why the premium?

Obviously, these price-to-earnings figures highlight that the stock isn’t cheap. However, there aren’t many companies on the FTSE 100 with double-digit earnings growth. It’s offering rare blue-chip exposure to such growth.

Equally, there aren’t many companies on the index that have such a strong moat. With operations in civil aerospace, defence, and power systems, Rolls operates in highly guarded and protected sectors.

Becoming a riskier investment

Rolls-Royce stock’s certainly becoming more expensive based on projected earnings. And there are multiple ways of looking at this.

Firstly, with all three of its businesses performing well, and investors pointing to potential in small modular reactors, there are a lot of positives to take.

However, expensive stocks can come crashing down if business performance or expected growth takes a turn. And that’s what potential Rolls-Royce investors should be wary of.

While these are all hypothetical, investors need to consider whether an end to the war in Ukraine would reduce long-term demand for defence products, or whether ongoing strikes — and the even longer downtime — at Boeing will impact demand for engines.

The bottom line

I think Rolls-Royce is less obviously undervalued than it has been over the past 18 months. While I’m still bullish on the business and continue to own shares in the company, I’m also cautious that there’s a long way to fall if Rolls’ earnings undershoot estimates.

This post was originally published on Motley Fool