The IAG (LSE: IAG) share price has rocketed 50.6% in the last 12 months. Investors who spotted its potential will either be thrilled they bought it, or kicking themselves for failing to do so. Sadly, I’m in the latter camp.

Like all the major airlines, British Airways owner IAG took a battering during the pandemic, with fleets grounded during lockdown. They still had to cover their huge fixed costs though, and most ran up hefty debts to do it. IAG’s forecast to end 2024 still owing £8bn. That’s only slightly below today’s market-cap of £10.5bn.

Net debt weighed on its share price even after people started to fly again. Given all the turbulence, it’s hardly a surprise IAG shares are still trading 36.8% lower than five years ago. However, this suggests there might still be a recovery opportunity here.

IAG shares have been among the cheapest on the FTSE 100 for some time now. Even after the recent turbo-charged run, they still trade at just 5.06 times trailing earnings. Only a handful of blue-chips are cheaper, as measured by their price-to-earnings (P/E) ratio.

Can this FTSE 100 stock continue to fly?

IAG also look good value measured by its price-to-sales (P/S) of 0.4. This suggests investors are paying 40p for each £1 of sales the company makes.

However, airline ticket prices have fallen lately, as demand stabilises but flight supply rises. Today’s operating margin of 11.9% is forecast to dip to 11.7%. So the skies aren’t completely clear.

Despite that, brokers remain upbeat. A hefty 25 analysts offer one-year price forecasts for IAG, setting a median target of 250.4p. That’s an impressive 16.46% increase from today’s 214p.

There’s always a wide range of forecasts, especially with so many brokers offering their views. The minimum target is 170p, while the maximum is 450p. That last prediction would see the IAG share price more than double. I’m not sure investors are going to be that lucky, but it’s nice to see a splash of optimism.

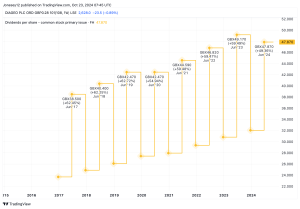

Good value and a rising dividend too

There was a lot to like in IAG’s first-half results. Sales climbed 8.4% to €14.7bn, although profit before tax dipped 1.1% to €905m. The board says the balance sheet’s “strong”, with liquidity jumping 42% to €9.7bn at 30 June.

Free cash flow hit €3.2bn and finally, the dividend’s coming back. It’s being restored at speed too, with a forecast yield of 2.87% for 2024 rising to 3.86% for 2025.

Much depends on the global economy, of course. China continues to struggle but there are hopes the US could engineer a soft economic landing. As ever, a natural disaster or regional war could smash the IAG share price overnight. Airlines are often on the front line of Black Swan events. A positive is that the oil price has been falling, cutting fuel costs. It could always start climbing though.

The early stage of any share price recovery is typically the best, and I’ve missed it. Yet over the longer run, I’d anticipate plenty of share price growth and dividends. Analysts are upbeat and IAG shares still look cheap. I’ll buy them as soon as I can put together the cash.

This post was originally published on Motley Fool