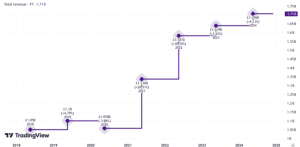

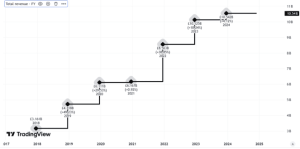

When a lot of us think about the shining stars across the pond in the S&P 500, our minds immediately go to Nvidia. This is for good reason, as the stock’s risen 152% so far in 2024. However, there’s one company that’s performed even better, gaining a whopping 259% in this calendar year. Let’s dig in.

Details to note

The company I’m referring to is Vistra Corp (NYSE:VST). It’s an integrated retail electricity and power generation company, noted as the largest competitive power generator in the US.

Vistra’s been around for several years, so some might wonder why the stock’s exploded 334% higher in the past year, particularly during 2024. The first boost came in late February, when it announced a strong set of results for the previous year. It reported net income of $1.49bn, a sharp turnaround from the loss of $1.21bn from the year before.

The business then benefitted from rising power prices. For example, natural gas prices have risen by 23% so far this year.

Yet the largest reason behind the move can be attributed to artificial intelligence (AI). This might seem odd for a utility provider. However, Vistra’s seen to be positioned to help provide nuclear capacity to power the energy-hungry AI processes. In fact, the share price jumped again last week following comments from the Alphabet CEO around how he’s looking to use electricity from nuclear plants to power its data centres.

Hold your horses

Simply put, AI’s potential market size is huge. The power needed to fuel the processes is even larger. So Vistra has a gold mine here on which to capitalise in coming years.

However, I do need to contain my excitement. The latest Q2 figures showed net income was broadly unchanged from the same quarter last year. The full financial benefit of AI won’t be felt for a while. In the report it noted that it had “started construction on two new solar facilities, a 200 MW site backed by Amazon in Texas and a 405 MW site backed by Microsoft in Illinois”.

These projects will take time to finish and come online. So there’s some risk that the share price could be in a bit of a bubble, with an investor frenzy pushing it higher before any clear benefit’s been enjoyed.

The bottom line

The Vistra performance has been incredible, but the rally has made the stock look a bit overvalued. The price-to-earnings ratio’s 107.9, well above the value of 10 I use for a fair value! Even for a growth stock it’s very high.

By comparison, other electric utility providers such as NRG Energy and and Exelon Corp have ratios under 20. This makes those stocks much more appealing to me.

Even though Vistra stock could keep soaring, I think I’ve missed the boat here. Therefore, I’d rather explore other stocks in the same sector that have a more reasonable value right now.

This post was originally published on Motley Fool