The Unilever (LSE: ULVR) share price has bounced back and the stock is doing what it does best — powering upwards whatever the weather.

Unilever shares are up over one week, one month, three months, six months and one year. They’ve grown a total of 24.53% in that time. It’s a brilliant turnaround after a difficult spell. In a sign of how badly it was doing, the shares are still down 1% over five years.

This suggests to me it’s not too late to participate in Unilever’s recovery by buying its shares. Or in my case, buying more of them.

Can the recovery continue?

I love picking out-of-favour stocks, where the underlying business is strong if only management can get a grip. That’s how I viewed Unilever, and things have panned out how I hoped. I wish it always worked out like that.

The consumer goods specialist threatened to collapse under its own weight after becoming an ill-focused, sprawling mess that had lost its focus on the bottom line. It’s picked itself up under new CEO Hein Schumacher but still has more work to do.

I bought the shares on 7 June last year at 4,000p. Today, they trade at just over 5,000p, and I’ve got a year’s worth of dividends too. I topped up my stake in both May and June this year, as my confidence in its recovery grew. Now I’m thinking of buying more.

Full-year 2023 results, published on 19 January, showed 7% underlying sales growth, rising to 8.6% for its 30 ‘power brands’.

A whopping 111% cash conversion rate and free cash of €7.1bn, up €1.9bn in a year before, also wowed. Unilever rewarded loyal investors with a new €1.5bn shareholder buyback and has started 2024 in fine fettle too. Underlying sales are up 4.1% while operating margins climbed 250 basis points to 19.6%.

FTSE 100 dividend growth stock

Life goes in cycles, and so do businesses. I think Unilever has further to go but there are threats. The US is flirting with recession. China’s in a right old mess. A global recession could eat into sales, volumes, cash flows and dividends.

Unilever shares aren’t as cheap as they were. I bought mine at a P/E of 18 times earnings. Today, that’s up to 22.93. So there’s less room for manoeuvre. Plus I’m also worried that Schumacher is yet to give the company the real shake-up it needs. I also fear some of its food brands are looking old hat. Bovril, Cornetto, Hellmann’s, Knorr, Pot Noodle and Viennetta are neither healthy nor cutting edge.

With a market-cap of around £125bn, Unilever is the third biggest stock on the FTSE 100, after AstraZeneca and Shell. If it climbed another 25%, that would push it past the £150bn mark.

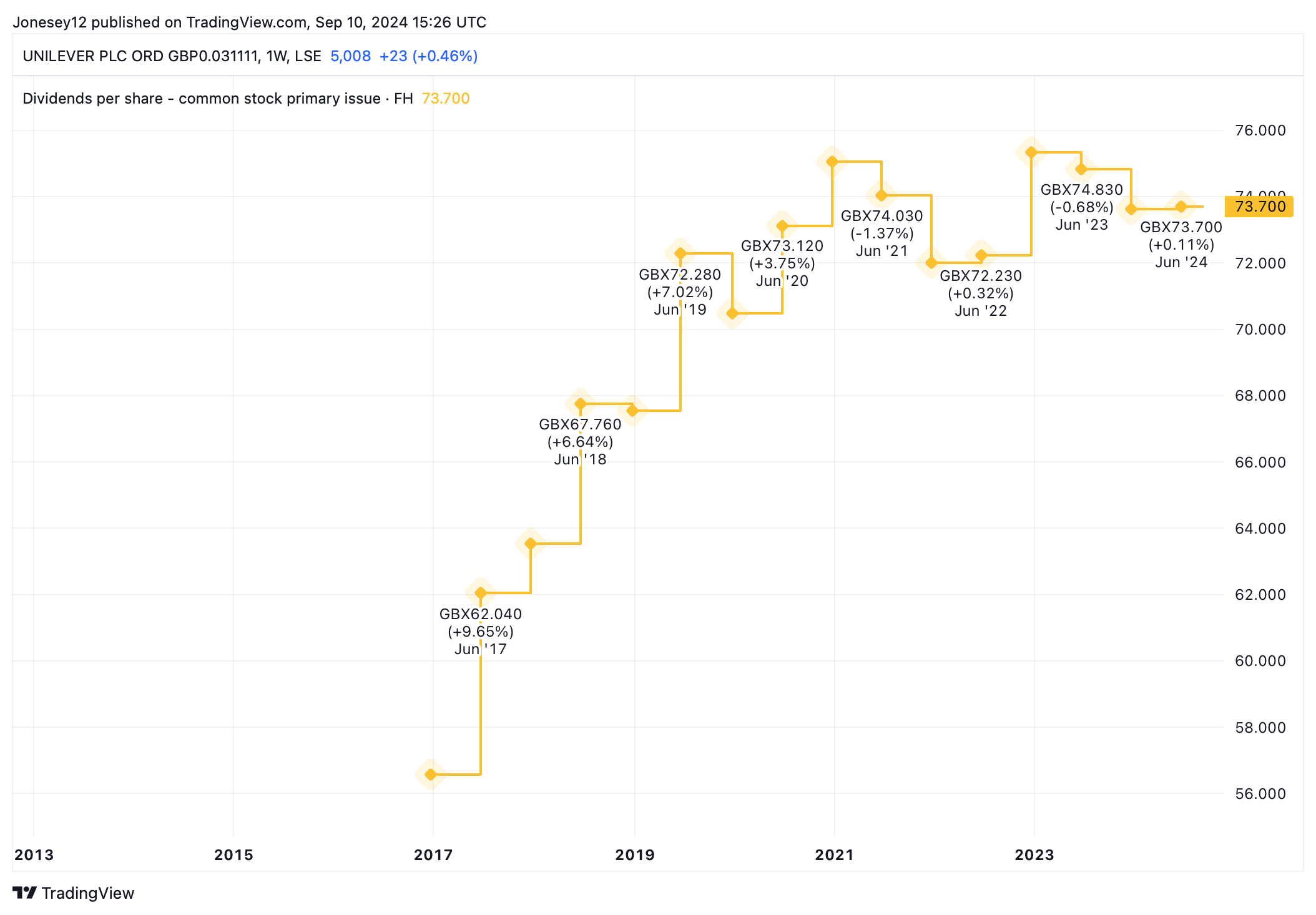

The air’s starting to get a bit thin up there. I wish it offered a slightly juicier yield than 2.97%. Worryingly, dividend per share growth has flattened out, as this chart shows.

Chart by TradingView

Which brings me to a technical problem. On 6 September, I received a dividend of £40. With the shares at £50, I don’t benefit from automatic dividend reinvestment. I therefore need to up my stake. Frankly, I can’t think of a better FTSE 100 stock to buy right now than Unilever. That’s what I’ll do.

This post was originally published on Motley Fool