The IAG (LSE: IAG) share price has rocketed 78.94% in the last two years, as it shrugs off the pandemic. Yet it still trades at a dirt-cheap valuation of just 4.21 times earnings, well below the FTSE 100 average of around 15 times.

Does that make this a bargain buy with more fuel in the tank, or something else?

British Airways-owner International Consolidated Airlines Group, to use its full name, continues to power ahead. Its shares are up 17.4% in the last 12 months.

Which brings me to my first problem. I prefer to buy top FTSE 100 stocks when they’re still struggling, in the hope of picking them up on the cheap and benefiting when they recover.

Cheap FTSE 100 opportunity

This isn’t a fool-proof strategy, though. I’ve bought both spirits giant Diageo and sportswear retailer JD Sports Fashion this year, shortly after both issued profit warnings. While JD Sports Fashion has kicked on, Diageo has been a bit of a downer.

Maybe it would be safer to buy a momentum stock instead, and IAG is certainly that. But why so cheap?

Investors are generally wary of airlines, which are at the mercy of hazards no management on earth can control, from volcanoes to warfare to oil prices. As the US, Europe, and China struggle economically, they’ve grown even more wary.

Even Ryanair has had a bumpy ride lately, as flattening seat prices hit profits. easyJet has just escaped relegation from the FTSE 100 by the skin of its teeth (having only rejoined in February). Shares in Wizz Air have plunged 45.7% over the last year. This is a volatile sector.

IAG ended 2023 with net debt of €9.25bn, which weighed on its valuation. However, the board has now cut that to €6.4bn. A first-half operating profit of €1.3bn, up €49m on last year’s bumper figure, brought further cheer.

Can IAG shares carry on climbing?

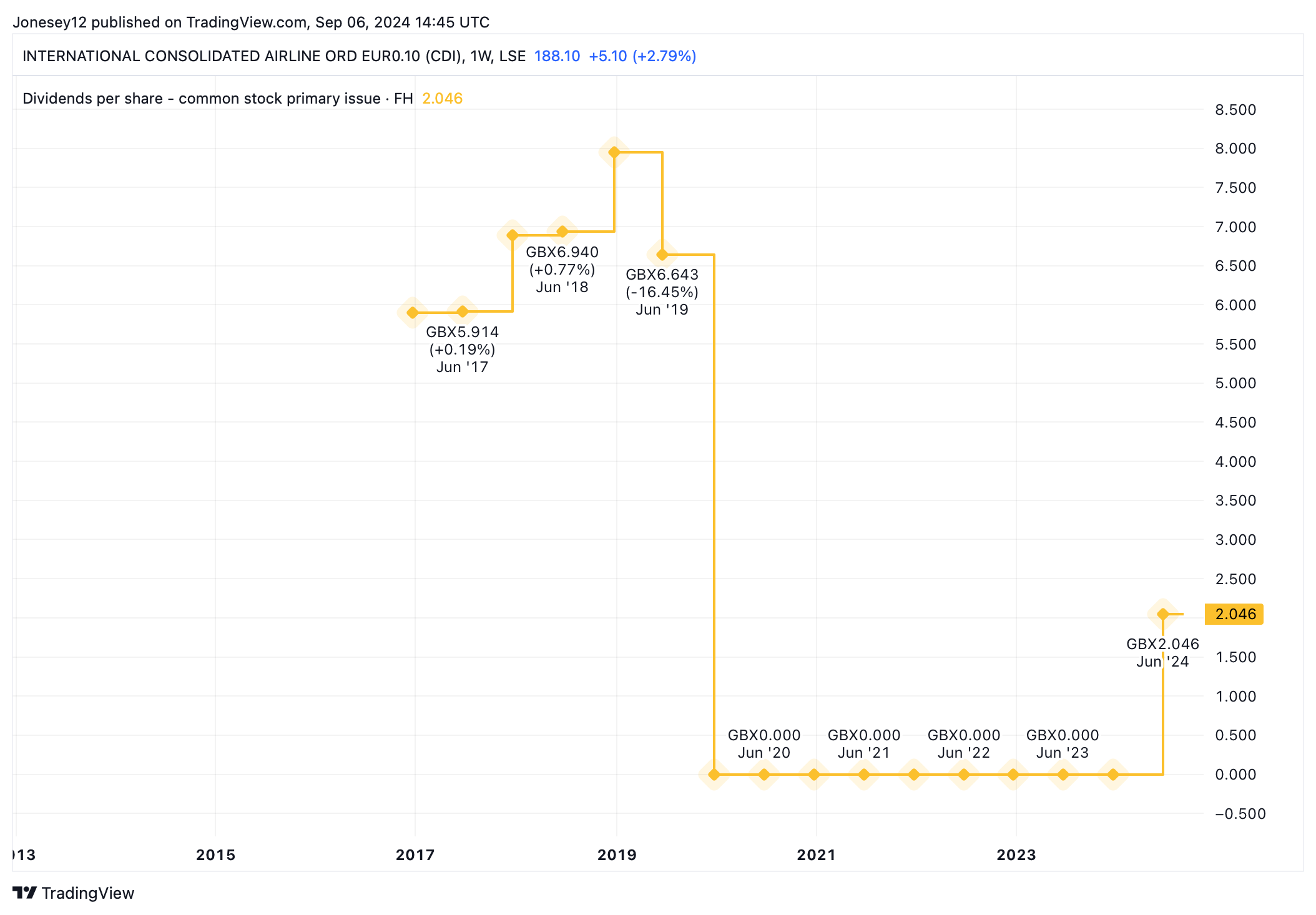

In another piece of good news, the board is set to restore the dividend. IAG shares are forecast to yield 3.29% this year, and 4.54% in 2025. That’s a pretty nifty recovery. This chart shows how they flatlined after the pandemic.

Chart by TradingView

The 16 analysts offering 12-month price targets for IAG have a median target of 227.64p. That’s up 20% from today’s 190p. They offer quite a broad range of estimates, though, from a peak of 447p to a low of 169p. The market still doesn’t quite believe in this stock.

That low P/E continues to baffle me. It’s based on last year’s earnings, but isn’t showing much sign of shifting. Earnings per share are forecast to rise a modest 2.67% over the next 12 months. The P/E looks set to remain low at 4.83 times earnings in 2024 and 4.62 times in 2025.

Today’s low P/E is not an automatic buy signal. It reflects high debt and external risks. I can imagine IAG shares hitting a spot of turbulence after their strong recent run. I’m seriously considering adding the stock to my portfolio, but it still makes me nervous. Am I missing something?

This post was originally published on Motley Fool