One FTSE 250 stock that caught my eye recently is TP ICAP Group (LSE: TCAP).

Here’s why I believe investors should consider snapping up some shares.

Diverse business

TP ICAP is a broking, data, and analytics business which serves some of the largest sectors in the world. These include financial services, energy, and commodities.

I can see that the shares have been on a fantastic run in the past 12 months. They’re up 43% from 166p at this time last year, to current levels of 238p.

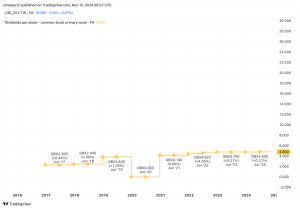

The investment case broken down

Starting with the bull case, on the surface of things, TP ICAP’s fundamentals look good. For example, the shares look decent value for money at present on a price-to-earnings ratio of eight. Plus, based on forecasts, the forward looking P/E ratio of 10 still indicates value ahead too. However, I do understand that forecasts don’t always come to fruition.

In addition to this, a dividend yield of 6.2% is attractive. However, I am conscious that dividends are never guaranteed. In addition to this, the business confirmed a share buyback scheme worth £30m earlier this month too, which is positive. It’s the third of its kind in the past 12 months.

Looking to the future, analysts expect earnings to increase by close to 70% next year. I’ll take these projections with a pinch of salt, of course. Nevertheless, it shows confidence at the very least.

Instead, I’d rather focus on TP’s most recent results. A half-year report released earlier this month made for good reading, in my view. Some of the key takeaways for me were that group revenue and EBITDA increased by 3% and 7%. Plus, earnings before tax and earnings per share rose by 10% and 8%.

Finally, I’m buoyed by TP’s data analytics business arm, Parameta Solutions. I reckon this is where the stock could see earnings growth and returns come from. The business is even considering a separate US listing, but I’ll keep an eye on developments closely. As the world continues along the digital revolution, there could be some exciting times ahead.

Risks and my verdict

From a bearish standpoint, it’s worth noting that the firm’s broking business may become obsolete in the future. This is due to changes in technology, and the fact people may move away from executing trades over the phone in favour of smarter ways of working. This could impact investor sentiment and returns. However, at present, the business continues to churn out decent earnings from this aspect of the business.

Next, from an income perspective, it’s hard to ignore the firm’s track record and balance sheet. It has had a chequered history of payouts, and debt levels at present are something I’ll keep an eye on. These debts could hinder returns, as well as growth initiatives.

Overall, there’s a lot to like about the business, in my view, including a decent valuation, as well as a passive income opportunity to kick things off. The ace up its sleeve is the data side of the business, which could have tremendous potential moving forward, and catapult the business to new heights.

This post was originally published on Motley Fool