Back in May 2022, I wrote that I was staying away from Diageo (LSE:DGE) shares. Since then, the stock’s fallen by around 35%.

This isn’t about me doing victory laps – I’ve had plenty of investments that haven’t worked out. But the recent decline in the Diageo share price makes a more important point for investors.

How much would I have?

In May that year, £1,000 would have bought me 26 Diageo shares. Today, that investment would have a market value of around £640, which isn’t a good return.

I’d also have received dividends during that time though. The company’s distributed around £1.59 per share, which means I’d have earned another £41.29.

Of course, I could have increased my earnings power by reinvesting the dividends along the way. But there’s no way around the fact I’d have lost money if I’d bought the stock in May 2022.

Things are different now though. I’ve been buying Diageo shares for my portfolio and I’m expecting the returns to be much better than the last couple of years.

What’s changed?

In a lot of ways, Diageo’s still the same as it was in 2022. The company still has an enviable portfolio of brands with leading products in several categories and its scale advantage remains unmatched.

The biggest difference is valuation. When I thought the stock looked expensive, it was trading at a price-to-earnings (P/E) ratio of around 27.

Diageo P/E ratio 2019-24

Created at TradingView

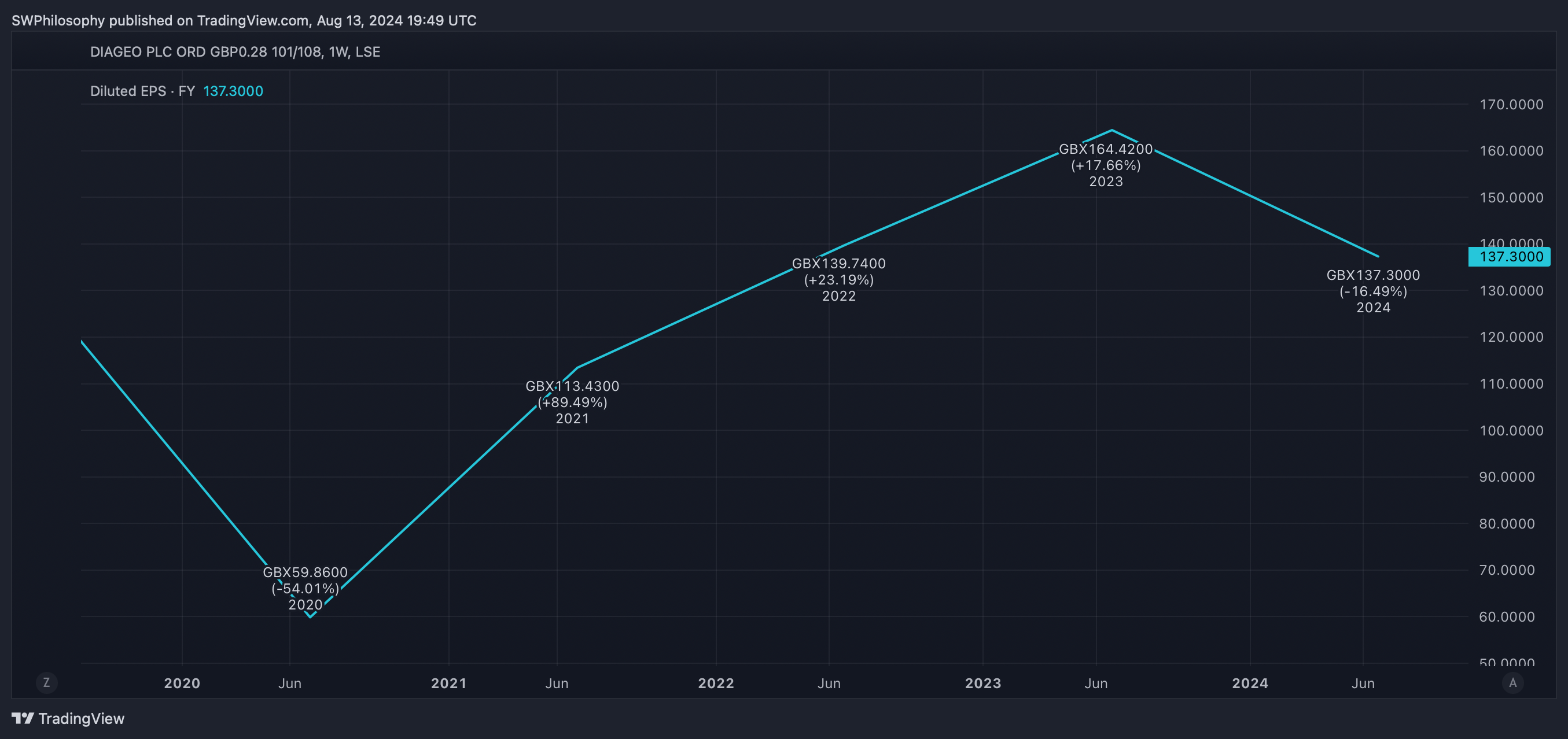

But this has fallen to around 17. In fact, that’s a big reason why the stock’s fallen over the last couple of years – earnings per share are roughly where they were.

Diageo earnings per share 2019-24

Created at TradingView

In other words, the business is making roughly as much money as it was in 2022, but the stock’s 35% cheaper. That’s why I think it’s attractive at today’s prices.

Why’s the stock been falling?

Diageo’s lack of earnings growth has been a big problem. Investors who bought the stock at a P/E multiple of 27 were probably hoping for better.

That’s why the stock’s been falling. But the main challenges have been external ones – difficult trading conditions and shifts in foreign exchange rates.

The last 18 months have reminded investors of the risks that come with owning Diageo shares. But I think what will matter over time is the company’s intrinsic strength, which is still very much intact.

The business still has quality brands in categories with high barriers to entry. And its ability to add new products to its portfolio and expand their reach with its network is a big long-term advantage.

Investing lessons

Paying too much for shares can lead to disappointing returns. But I think even investors who are down 35% today will do fine over time with a quality company like Diageo.

That said, I’d much rather buy the stock at today’s prices. It’s absolutely possible the share price could fall further, but at a P/E ratio of 17 it looks like much better value than it was in May 2022.

This post was originally published on Motley Fool