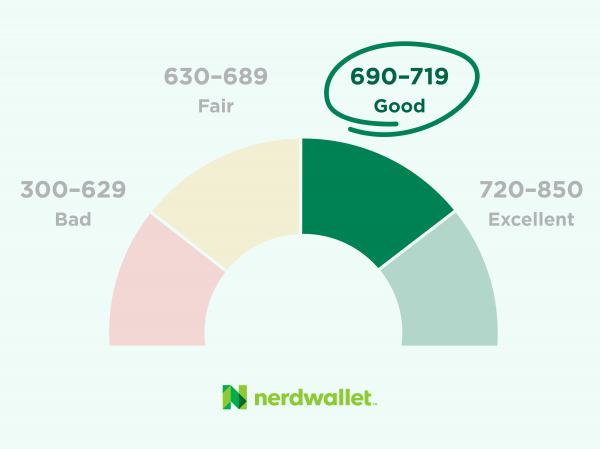

A credit score of 715 puts you at the top of the “good” band (690-719) on the generally used credit score range of 300 to 850 and well on your way to the “excellent” band with a bit of work and extra attention.

With a 715 credit score, you’re likely to qualify for a wide range of financial products and services, although reaching that excellent category will help you land lower interest rates and even better deals, saving you money in the long run.

Still, a 715 score is something to celebrate, especially if you’ve made improvements to your previous score to get there. Here’s how you compare:

-

With a 715 score, you are on par with the average FICO 8 score of 716, as of the second quarter of 2021, and much higher than the VantageScore 3.0 average of 695 during the same period.

-

A 715 score puts you just 5 points away from the excellent range, so it’s important to stay mindful of the factors that make up your score to hold your ground or, even better, build and hit the next band.

What a 715 credit score can get you

The better your credit score, the easier it is to qualify for loans, credit cards, and other financial products and get good terms like low-interest rates. When reviewing your application, lenders consider your credit score, among other factors like your debt-to-income ratio, the length of your credit accounts and your payment history.

So, while your credit score is just one factor among many, it holds a lot of weight and is often seen as a way to predict your “creditworthiness,” or your ability to pay back the money you’ve borrowed.

Although a 715 credit score doesn’t necessarily guarantee eligibility for a loan or a low-interest rate, here’s what you can generally expect as someone with solidly good credit:

Car loans

If you’re planning to buy a car — new or used — it’s a good idea to make sure your credit is in top shape before you hit the dealership. In fact, your credit score is likely the most significant factor in what interest rate you’ll get. A 715 score puts you in the “prime” category, according to Experian, which collects data about auto financing in its annual State of the Automotive Finance Market report. This means you are likely to receive an auto loan interest rate of 3.64% for a new car and 5.35% for a used car, which aligns with the national average as of the third quarter of 2021.

According to the same Experian report, the average credit score for a new-car loan in 2021 was 733 and 675 for a used-car loan. A 715 score is lower than the average for new-car buyers but significantly higher than the average score of people who purchased used cars.

Ultimately, a 715 credit score will not be a barrier to purchasing a car, but it won’t secure you the best annual percentage rates — those below 3% for a new car — which will likely go to people with a score above 780.

Home loans

One of your home loan application’s most significant and essential pieces is your credit score. Borrowers with a 620 credit score should typically qualify for a conventional loan, but those with a 740 or higher will likely get a better interest rate. With a 715 score, you’re well above that bottom line but still won’t get the lowest rates.

Conventional loans are a great option for buyers who can put down at least 3% on a home, but a 715 score could also qualify you for an FHA, VA or other government-backed mortgages.

Credit cards

A 715 score near the top of the good range will likely give you many options when searching for credit cards. For example, cards offering rewards or cash back will likely require good or excellent credit for approval.

Applying for a credit card can ding your score in the short term, so do your research and make sure that the card fits your needs and you have a good shot of being approved.

Personal loans

While there is some variation, the consensus among lenders is that borrowers should have a credit score in the good or excellent range (690 and above) to qualify for a personal loan. With a 715 score, you’re securely in that window, but your interest rate will not be as low as someone with a credit score in the excellent range.

Strategies to keep building your 715 credit score

It’s hard to improve your credit if you don’t know what factors go into the overall calculation. While credit scoring can seem a bit mysterious, there are some proven practices that will polish your score with a bit of patience and consistency.

Pay on time

A long record of solid payments is one way to make your credit file stand out, which means paying your balances on time and in full is crucial. Missing a payment by 30 days or more can slash your score by 100 points, so take those due dates seriously. Set up autopay or add calendar reminders if they’re hard to remember.

Don’t use all the credit available to you

Your credit utilization ratio, or how much you owe on all of your credit accounts in relation to your total available credit, is one way your creditworthiness is assessed. If your utilization is too high, you seem riskier to potential lenders.

Focus on using about 30% of your credit limit — 10% is even more ideal. So if your credit limit is $1,000, try to keep your balance below $300.

Keep your accounts open — especially your oldest

As counterintuitive as it might seem, keeping your oldest credit account open — even one you don’t use often — strengthens your credit score. Potential lenders look at the age of your credit: The longer you’ve had credit in your name, the better. Rather than close out that unused credit account, try using it for regular but inexpensive purchases such as a streaming subscription or a cup of coffee. This way, you keep the account in use but know you can pay off the balance easily each month.

Be strategic about new credit applications

Every time you apply for a credit card or loan, it can cause a dip in your score, even if it’s only temporary, but too many applications at once can make the damage worse. So space out your credit applications — one every six months is a good guideline — to keep your score steady.

What happens to a 715 score with a late payment?

It’s not realistic to think you’ll never miss a due date, but when you do, try to pay the balance right away if you can. If you’re a few days late, it won’t impact your credit score. The actual harm is being more than 30 days late because, at that point, the missed payment is likely reported to the credit bureaus. You could see a potential drop in your score by as much as 100 points, which would take you way out of the good range.

Get score change notifications

See your free score anytime, get notified when it changes, and build it with personalized insights.

This post was originally published on Nerd Wallet