I’m searching for the best penny stocks to buy as I target big capital gains and a healthy passive income. Here are two of my favourites that I feel are worth considering.

Good Lord!

Lords Group Trading‘s (LSE:LORD) a specialist supplier of building, plumbing, heating and DIY products in the UK. This gives it good scope to grow profits as housebuilding activity accelerates (Labour has set a goal of 300,000 new homes by 2029).

But this isn’t all. The AIM-listed company’s focused on repairs, maintenance and improvement (RMI), a market from where it sources around 80% of revenues. Given that the UK has the oldest housing stock in the world, Lords can expect strong and sustained revenues from now and into the future.

Finally, I believe its robust balance sheet gives Lords a chance to bolster earnings growth through further acquisitions. Its expansion strategy saw it hoover up another two companies in 2023 — Chiltern Timber Supplies and Alloway Timber — taking the total number of acquisitions to seven in 15 years.

City analysts are predicting Lords’ profits column to swell in the next few years. Bottom-line growth of 156% and 33% is forecast for 2024 and 2025. This also builds expectations of more healthy dividends, leading to a 4.7% dividend yield through to the end of next year.

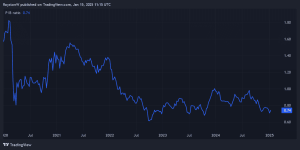

Lords’ share price has fallen steadily in recent years as a result of high interest rates. Like-for-like revenues here dipped 1.2% in 2024 due to difficulties in the construction sector.

Further trouble could be in store if the Bank of England fails to meaningfully cut interest rates. But with inflation falling and the central bank already loosening monetary policy, the omens are looking increasingly good for this penny stock.

All-round value

Brickmaker Michelmersh Brick Holdings (LSE:MBH) is another AIM stock that should benefit from a potential homebuilding boom. It also stands to gain from strong revenues to update Britain’s ageing homesteads. The company makes more than 125m clay bricks and pavers each year.

I especially like this business because of the excellent all-round value it offers. The firm trades on a forward price-to-earnings (P/E) ratio of 9.4 times, which is much lower than those of industry rivals Forterra and Ibstock.

Michelmersh also offers up a tasty 4.7% dividend yield today. It’s tipped to continue growing dividends over the forecasted period too.

Those targeting immediate earnings growth might be disappointed however. Earnings are tipped by City analysts to drop 13% in 2024, before rising 4% and 5% in 2025 and 2026 respectively.

Earnings projections here could, as with Lords Group, be in peril if building activity remains under pressure. On top of this, Michelmersh’s vulnerable to a sharp uptick in costs across its six factories if energy prices soar. Brickmaking is a notoriously power-intensive task.

Still, on balance, I believe the potential long-term benefits of owning this penny stock outweigh these risks, and especially at current prices.

This post was originally published on Motley Fool