There are hundreds of dividend stocks for British investors to choose from in the FTSE alone. And it’s an advantage that many international investors aren’t fortunate to have. After all, the London Stock Exchange is home to some of the most lucrative income opportunities in the world.

Sadly, not all dividends are equal. Hunting high-yield opportunities is simple enough. Yet these often have a habit of turning into traps that generate some passive income in the short term but fail to keep up in the long run. Don’t forget dividends are funded by excess cash flow. And should that stream of money become compromised, shareholder payouts tend to follow suit.

With that in mind, there are currently two seemingly popular income-generating businesses that I wouldn’t touch.

A new type of insurance

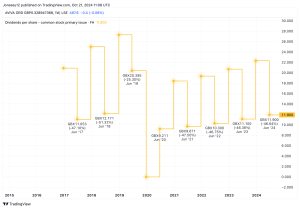

Phoenix Group Holdings (LSE:PHNX) has been a terrific performer over the years and is currently offering a jaw-dropping 10.2% yield!

The insurance firm rose to prominence with a fairly simple business model – buy redundant life insurance and let the contracts run. A lack of interest from other insurance giants enabled Phoenix to operate with minimal competition. And it’s a tactic that generated ample cash flow with minimal claim payouts to customers, translating into juicy dividends.

The problem is that as a result of Phoenix’s success, the firm’s grown far too large for this strategy to remain effective. As such, management’s now transitioning away from this strategy and is going to have to compete with insurance titans like Aviva.

The company has little experience in this new domain. And if it can’t carve out a niche for itself, today’s impressive yield might well soon evaporate.

Leveraged telecommunications

Vodafone‘s (LSE:VOD) been a pretty abysmal performer over the last five years. The telecommunications giant’s struggling under the weight of its debt pile now that interest rates have gone through the roof. And we’ve already seen the yield slashed in half — from 10.1% to 5.1% earlier this year.

Yet even at this reduced payout, the shares seem to remain popular among income investors. To be fair, there’s some optimism to be had around a potential turnaround play. The new CEO’s streamlining operations and disposing of non-core assets to reduce the burden of leverage while also refocusing efforts to improve performance in core markets.

Yet earnings are still moving in the wrong direction. And if efforts to right the ship fail, this dividend stock could see its yield cut once again, with the share price falling even further. Yet there have been some encouraging early signs of progress. But given this isn’t the first time management’s promised to deliver a better performance, I’m not willing to give it the benefit of the doubt.

This post was originally published on Motley Fool