I think we could be in for a great decade for passive income investing. And I think I see some super cheap buys that might not remain that way for much longer.

Buying stocks and shares to target long-term passive income caries risk. And right now, a Cash ISA paying 5% a year could be just right for those who don’t want that risk.

It can’t last

But returns from cash have to fall when the Bank of England cuts its rates. And by the time they’re down significantly, might a lot of today’s stock market bargains be gone?

For me, it’s worth taking the extra risk based on the long-term outperformance of the stock market. But I’d be in it for a minimum of 10 years, to make it a bit safer.

With that said, I’d rate my first passive income pick as maybe among the FTSE 100‘s risker ones, at least in the medium term.

Rising dividends

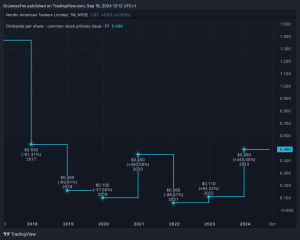

I’m talking of Legal & General (LSE: LGEN) with its fat forecast 8.7% dividend yield. The yield might not last if the Legal & General share price makes much progress. For now though, it hasn’t been moving much. And it’s still down 15% in the past five years.

I suspect part of the share price weakness is down to a forecast price-to-earnings (P/E) ratio of 10.7. Coming after a 2023 in which earnings crashed, that might be seen as not that cheap for an insurance and investment company, which is prone to cyclical ups and down.

Earnings growth

But those forecasts show earnings growing, and the P/E dropping. And the dividend looks set to grow, if slowly.

In this sector, I expect more risk and volatility in the short term. So Legal & General, even more than most, would have to be a decade-plus hold for me.

But I reckon it can provide solid long-term income, if perhaps a bit erratic from time to time.

Supermarket power

I’m turning to the FTSE 250 next, and a real estate investment trust (REIT). It’s Supermarket Income REIT (LSE: SUPR), with an 8.3% forecast dividend yield.

The share price is down 30% in five years, after the real estate slump.

I like the thought that Tesco, the UK’s biggest supermarket chain, looks set to pay a 3.9% dividend. But this REIT, which counts Tesco as one of its biggest tenants, pays more than twice as much.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice.

Real estate

What happens next will depend on the property market, and retail real estate could remain weak for a lengthy period. Earnings forecast for the current year are poor, as the REIT comes back from a 2023 loss. And that could keep the share price low for longer.

But if forecasts come good, we could see earnings storm back in 2025 for a P/E of only 7.5. And a steady dividend that could trounce Tesco’s.

Two to buy?

I don’t know which passive income stock I’ll buy next, as I see so many good candidates. But these two are on the list.

This post was originally published on Motley Fool