The best investment opportunities aren’t always obvious. There’s a UK stock I’m looking to buy at the moment that I suspect a lot of investors won’t have heard of.

With a market-cap of £295m, Porvair (LSE:PRV) isn’t a member of the FTSE 100 or the FTSE 250. But I think it’s an extremely impressive business trading at a price that looks like an opportunity.

What’s the company?

Porvair manufactures specialist filtration equipment for aerospace, laboratory and metal melting. And there’s a lot to like about the way it operates.

The company’s products are critical for end users. Combined with strong relationships with its customers and a reputation for quality, this makes the business extremely difficult to disrupt.

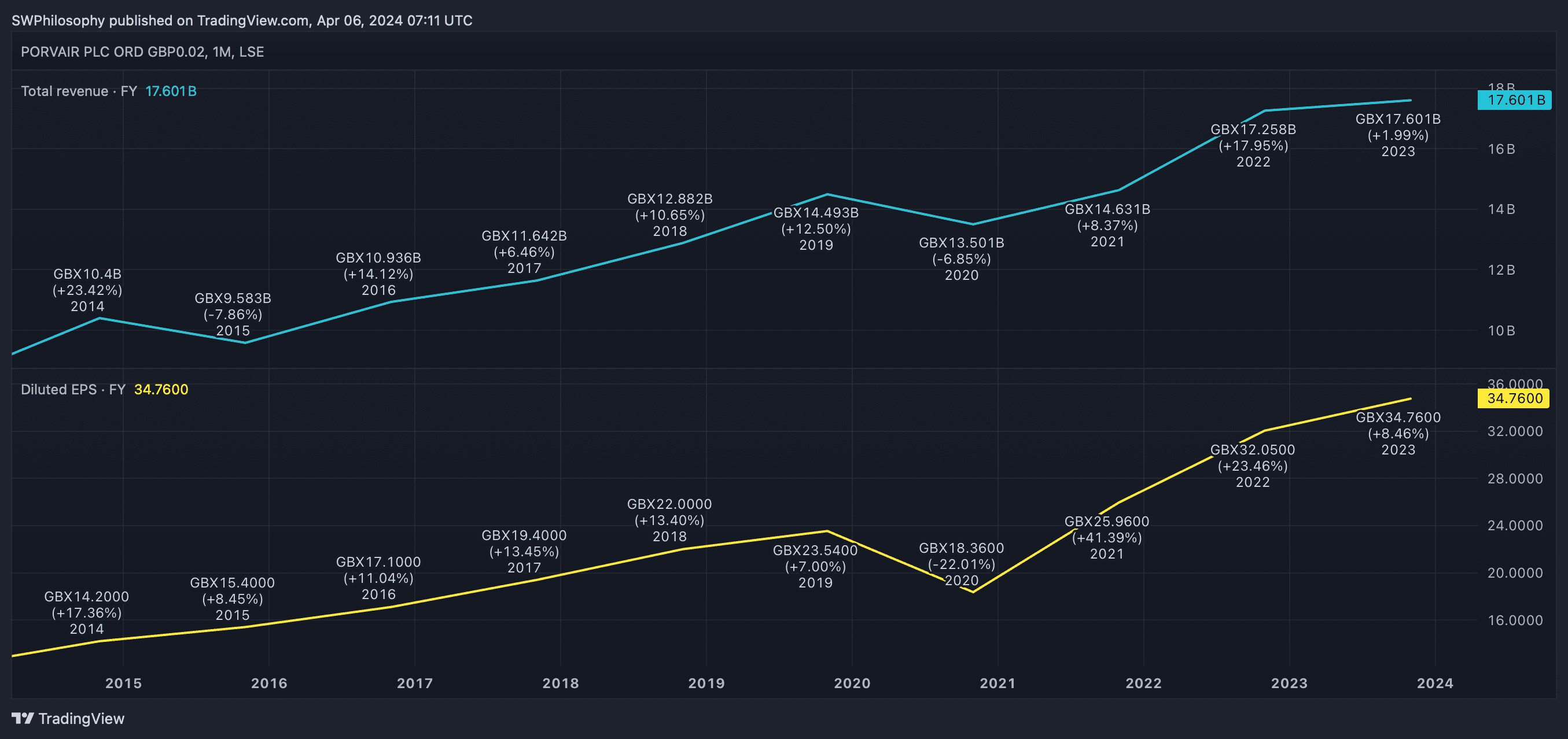

Porvair revenue and profit 2014-24

Created at TradingView

Porvair’s strong competitive position is reflected in its financial performance. Over the last 10 years, the company’s revenues have increased 73% and earnings per share are up 150%.

This is during a period that has had some significant macroeconomic challenges. But even Covid-19, high inflation and a recession haven’t been able to halt the firm’s progress in any meaningful way.

A bargain price

It reminds me of Halma and Diploma, which I consider to be some of the best companies in the FTSE 100. It isn’t quite in that league when it comes to cash generation, but I think it’s similar.

The company’s strategy of occupying niche industries matches Halma’s business plan. And its focus on mission-critical equipment and components is straight out of Diploma’s playbook.

Importantly though, the stock trades at a much lower valuation. Where Halma and Diploma both trade at price-to-earnings (P/E) ratios above 35, Porvair shares are at an earnings multiple of 18.

Porvair P/E ratio 2014-24

Created at TradingView

That’s low compared to its bigger counterparts and it’s low compared to its historic levels over the last decade. Importantly, I think it’s also a bargain relative to the company’s intrinsic value.

Risks

There are risks with every business and Porvair’s no exception. As a manufacturing company where capital expenditures account for around 25% of operating cash flow, inflation can be a threat.

In addition, the industries the company sells into – notably aerospace and laboratories – are highly cyclical. So there’s the possibility of demand declining in difficult conditions.

Importantly, Porvair has actually handled both of these risks quite well of late. In terms of inflation, the company’s reputation for quality has helped it keep growing to offset cost increases.

Furthermore, while its end markets are cyclical, they are also diversified. Higher lab activity during the pandemic offset a decline in air travel and the reverse has been true since.

Under the radar?

The fact Porvair isn’t big means it probably doesn’t get the coverage from analysts it deserves. But that’s absolutely fine by me – I’m happy to buy it even if others are just talking about it.

I think there’s an opportunity right now to buy shares in an exceptionally good company at an unusually good price. That’s why I’m looking to add it to my Stocks and Shares ISA this month.

This post was originally published on Motley Fool