hVIVO (LSE: HVO) was a penny stock when I first bought it at 11p in late 2022. By July 2024, it spiked at 30p and I was sitting pretty (or so I thought).

The market cap had also surpassed £200m by then, disqualifying it from being called a penny stock. In the UK, those are often seen as stocks with a market cap under £100m as well as a share price beneath 100p.

Now, as I write (26 December), the share price has pulled back sharply to 19.56p. I’m still up, but I also bought shares in the summer at 29p and that purchase is down sharply too.

To be fair, I knew what I was getting myself into, as small-caps and penny stocks are prone to stomach-churning bouts of volatility. This one’s certainly been no exception to the rule.

Yet I’m ready to take one last nibble on hVIVO shares in early January. Here’s why.

What is hVIVO?

For those unfamiliar, hVIVO is a firm that specialises in human challenge trials (HCTs), a growing niche market within the massive contract research organisation industry.

HCTs involve deliberately infecting healthy volunteers with a pathogen in a controlled environment to test treatments. The firm recruits these paid volunteers — many of them students in need of some cash — through its own FluCamp business.

hVIVO works with four of the top 10 global pharmaceutical companies. It conducted the world’s first Covid HCT during the pandemic, generating data that advanced understanding of the virus and helped guide vaccine development.

However, ‘vaccine’ has become a bit of a dirty word in some quarters following the US election.

Dark clouds

In November, Donald Trump nominated vaccine-sceptic Robert Kennedy Jr to lead the Department of Health and Human Services. We don’t know whether he’ll get the gig, but the market isn’t waiting to find out. The hVIVO share price is down 30% since then.

The fear seems to be that if major pharmaceutical companies anticipate a hostile regulatory or funding environment under Kennedy, they might reduce investments in vaccine-related projects. This could affect hVIVO’s pipeline of contracts and growth trajectory.

But the future still looks sunny

The truth is we don’t yet know how things will play out. What we do know however is that the company recently signed an £11.5m contract with an unnamed blue-chip pharmaceutical client to test a new antiviral candidate for respiratory syncytial virus (RSV).

This virus affects around 33m people annually, leading to approximately 4m hospitalisations worldwide and 101,000 deaths in children under five years old.

CEO Yamin ‘Mo’ Khan commented: “This contract further demonstrates the trust and confidence that leading pharmaceutical companies place in hVIVO’s human challenge study models.”

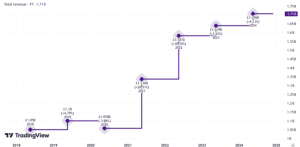

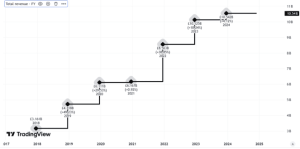

The study is scheduled to commence in H2 2025, with revenue recognised across 2025 and 2026. For 2024, management expects revenue of £62m, with a healthy EBITDA margin of around 22%-24%. And it’s targeting £100m in revenue by 2028.

hVIVO is an industry leader in human challenge trials, a market which is expected to grow from $100m-$150m today to as much as $1bn in the years ahead.

The business is highly cash generative and debt free. It’s even started paying a small dividend.

Lastly, with the stock on a forward price-to-earnings multiple of 11.7, the valuation looks very attractive.

This post was originally published on Motley Fool