Shares in Rentokil Initial (LSE:RTO) have consistently underperformed the FTSE 100 over the last few years. But I’ve high expectations for the stock in 2025.

My investment thesis has two parts. The first is the price-to-earnings (P/E) multiple the stock‘s trading at. And the second is that the underlying business is showing signs of recovery.

Valuation

Rentokil shares currently trade at a P/E multiple of 26. That doesn’t look particularly low, especially compared with the FTSE 100 trading at an average P/E of around 15.

There are however, a couple of things worth noting. The first is the company might well be better than the average FTSE 100 business – for one thing, it’s in an industry that’s growing steadily.

More importantly, a P/E multiple of 26 is actually unusually low for Rentokil shares. Since the pandemic, the stock’s traded at an average P/E ratio of around 35.

Rentokil Initial P/E ratio 2020-24

Created at TradingView

This indicates investors are less optimistic about the business than they have been for some time. But if that changes and the P/E gets back its recent average, the share price could climb 35%.

By itself however, this isn’t a good enough reason to consider buying the stock. If the stock takes years to recover, it might still underperform the FTSE 100 as the index rises faster.

What the stock needs is a boost from the underlying business. And I think this might be coming in 2025.

Time to shine?

Over the last couple of years, Rentokil’s been struggling with the integration of Terminix – a US rival it acquired in October 2022. The main effects of the acquisition so far have been higher costs.

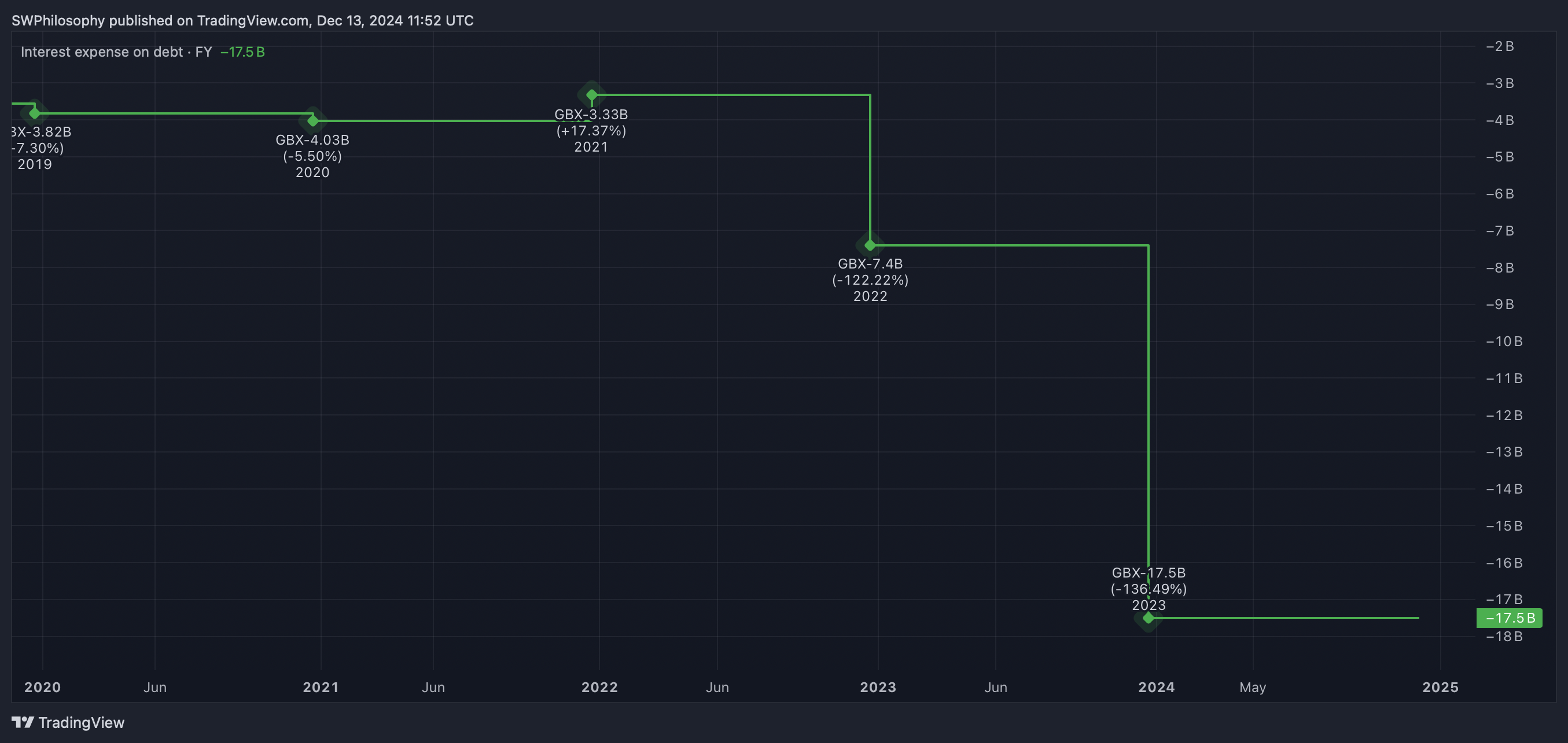

Rentokil Initial Interest Expense 2020-24

Created at TradingView

As a result of its net debt more than doubling, the company’s been facing higher interest payments. And this is an ongoing risk for shareholders.

To date, investors haven’t had much to show for this. But the firm’s latest trading update indicated that rewards could be on the way.

In October, Rentokil set out its clearest plan for generating efficiencies to date. This includes integrating branches, re-routing technicians, and migrating data and information systems.

The company‘s been implementing these changes over the last three months and intends to assess them in early 2025. So I’ll be watching the March and April updates with interest.

If the cost-saving initiatives are starting to take shape, I think margins could expand and profits could pick up sharply. And this could have a very positive effect on the share price.

Activism

The Rentokil share price has been volatile in 2024. And more than one of the big rises have been the result of activist investors taking an interest in the stock.

This isn’t something I’d bank on. But an unusually low valuation and a business making progress is enough for me to think investors should consider buying the stock for 2025 and beyond.

This post was originally published on Motley Fool